Time for a North Carolina geography quiz!

In which counties are these cities located: Chapel Hill, Durham, and Raleigh?

If you said Orange County, Durham County, and Wake County, you are . . . only partially correct. Each of those cities lies in two counties. These municipalities and the many others in North Carolina that cross county lines face a variety of challenges relating to property taxes. For starters, these cities need to work with multiple county assessors to determine their tax bases. If they don’t collect their own property taxes, these cities need to contract with multiple county tax collectors for that service. Individual real property parcels that are in the city but lie in two counties create additional assessment and collection headaches.

Today’s post focuses on another potential property tax difficulty faced by multi-county municipalities: calculating the revenue-neutral property tax rate (“RN rate”). The RN rate, which is intended to help citizens compare a jurisdiction’s property tax rates before and after a property tax revaluation, must be calculated whenever real property in the jurisdiction is reappraised by a county.

A city that lies in multiple counties must calculate a new RN rate whenever any of those counties conducts a revaluation. High Point, for example, lies in four (!) counties: Davidson, Forsyth, Guilford, and Randolph. Whenever any one of those four counties conducts a revaluation, High Point must recalculate its RN rate.

[For more background on the RN rate and the required calculations, please see this blog post and this bulletin.]

In addition to needing to calculate its RN rate more frequently, a multi-county municipality faces a particular challenge with that portion of the RN calculation that requires the municipality to determine the growth rate of its tax base in between county revaluations. This growth is the “regular” increase in a city’s tax base due to new construction and purchases of equipment, cars, and other taxable personal property.

For a one-county city, the growth rate calculation is relatively simple. The city determines the change in its tax base in between each non-revaluation year and then averages those changes to get its overall growth rate since the last revaluation. In other words, the city calculates the average increase or decrease in its tax base between years in which the county does not conduct a revaluation.

For example, assume Blue Devil City lies only in Carolina County. The county is on a 4-year revaluation cycle, with revaluations in 2017 and 2021. The city must therefore calculate its RN rate for 2021 (meaning the fiscal/tax year that runs from July 1, 2021 to June 30, 2022). As part of that calculation, the city needs to determine its growth rate in between Carolina County revaluations. Here are the city’s tax base data for the relevant years:

2017: $1,000,000,000*

2018 : $1,015,000,000

2019: $1,040,000,000

2020: $1,060,000,000

2021: $1,400,000,000*

(The years 2017 and 2021 have asterisks because they are the county revaluation years.)

Because the county is on a 4-year revaluation cycle, the city must calculate the non-revaluation-related growth for 3 pairs of years: 2017-2018, 2018-2019, and 2019-2020. The city will not calculate a growth rate for from 2020 to 2021 because 2021 is a revaluation year; the change in the tax base from 2020 to 2021 is due (mostly) to the revaluation and not regular growth from new construction and purchases of new equipment, etc.

[As I discuss in this bulletin, the growth rate calculation for cities can get more complicated if there are annexations or other one-time events with material impacts on the city’s tax base. Let’s assume that’s not the case for Blue Devil City.]

Here are the 2021 growth rate calculations for Blue Devil City:

2017 to 2018: ($1,015,000,000 - $1,000,000,000) / $1,000,000,000 = 1.5%

2018 to 2019: ($1,040,000,000 - $1,015,000,000) / $1,015,000,000 = 2.4%

2019 to 2020: ($1,060,000,000 - $1,040,000,000( / $1,040,000,000 = 1.9%

The city then averages those three percentages to get its overall growth rate since the last county revaluation:

(1.5% + 2.4% + 1.9%) / 3 = 1.93% Growth rate used for 2021 RN rate calculation

Easy peasy, right?

Let’s see how this calculation changes for municipalities that lie in more than county.

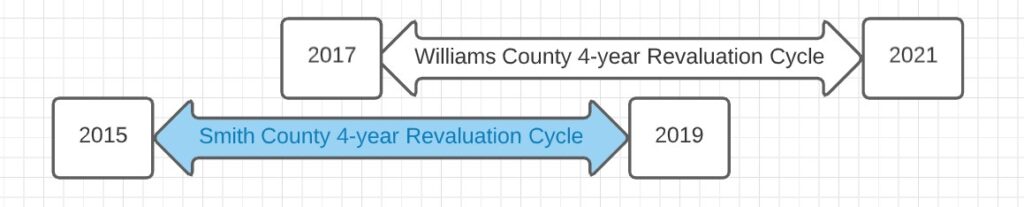

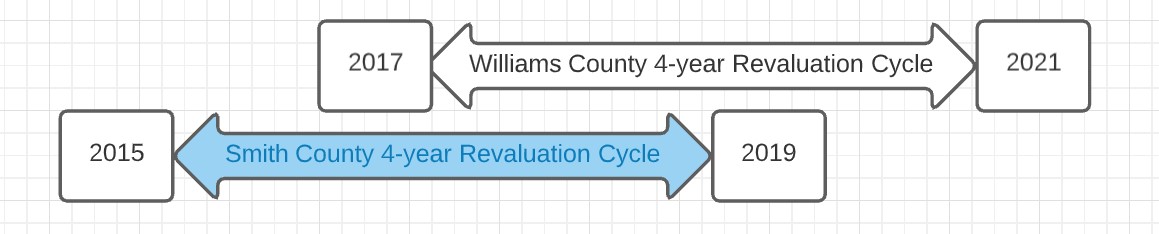

Assume that Tar Heel Town lies in 2 counties, Williams County and Smith County. Williams County is on a 4-year revaluation cycle, with revaluations in 2017 and 2021. Smith County is on a different 4-year cycle with revaluations in 2015 and 2019.

Here are the town’s tax base data needed to calculate its growth rate for the 2021 Williams County revaluation:

2017: $1,000,000,000* (Williams County revaluation)

2018 : $1,015,000,000

2019: $1,300,000,000* (Smith County revaluation)

2020: $1,340,000,000

2021: $1,700,000,000* (Williams County revaluation)

When calculating the 2021 RN rate for the Williams County revaluation, normally the town would look back to the last Williams County revaluation in 2017 and calculate three growth rates (2017 to 2018, 2018 to 2019, and 2019 to 2020).

But…notice that the change in the town’s tax base from 2018 to 2019 reflects not only regular growth (new construction, purchase of new personal property, etc.) but also the effect of the Smith County revaluation. If we calculated the growth rate back to the last Williams County revaluation in 2017, that calculation would include growth of 28% from 2018 to 2019, a huge percentage and clearly far more than we’d expect from regular growth. Including the impact of the Smith County revaluation would dramatically inflate the town’s growth rate for its 2021 RN rate calculation, which in turn would dramatically inflate the town’s 2021 RN rate.

To avoid that mistake, a multi-county municipality should calculate its growth rate back to the last revaluation by any county in which the municipality lies, not back to the last revaluation by the county that conducted the current revaluation.

In our example, that would be the 2019 revaluation by Smith County. When calculating the town’s 2021 RN rate after the 2021 Williams County revaluation, the town will calculate only one growth rate: 2019 to 2020. The town will not calculate growth rates prior to 2019 because they predate the most recent prior revaluation by any of its counties. Nor will it calculate the growth rate from 2020 to 2021 because that increase reflects the impact of the 2021 Williams County revaluation.

Under this approach, the 2021 Tar Heel Town growth rate would be:

2019 to 2020: ($1,540,000,000 - $1,500,000,000) / $1,500,000,000 = 2.67%

For multiple-county municipalities, the most recent revaluation is often one conducted by a county different from the county conducting the current revaluation (as in the case of Tar Heel Town above). But not always. If the revaluation cycle of one of those counties is contained entirely within the other county’s revaluation cycle, the growth rate can be calculated as usual.

Pretend that Wolfpackville is in both Red County and White County. Red County is on an 8-year revaluation cycle, with revaluations in 2015 and 2023. White County is on a 4-year revaluation cycle, with revaluations in 2017 and 2021.

When Wolfpackville calculates its RN rate for the 2021 White County revaluation, it will calculate its growth rate back to the 2017 White County revaluation. That calculation will be the same as we completed for Blue Devil City in the first example: averaging the growth between 2017-2018, 2018-2019, and 2019-2020. The town does not need to worry about a Red County revaluation affecting its 2021 RN calculation because Red County has not conducted a revaluation since the last White County revaluation.

Have you run into other difficulties when calculating your jurisdiction’s RN rate? Please share your experiences in the comment section below.