Having received lots of emails and phone calls after my earlier post on this topic, it seems worthy of a sequel. Here’s a few of the more interesting questions from across the state this past week.

Having received lots of emails and phone calls after my earlier post on this topic, it seems worthy of a sequel. Here’s a few of the more interesting questions from across the state this past week.

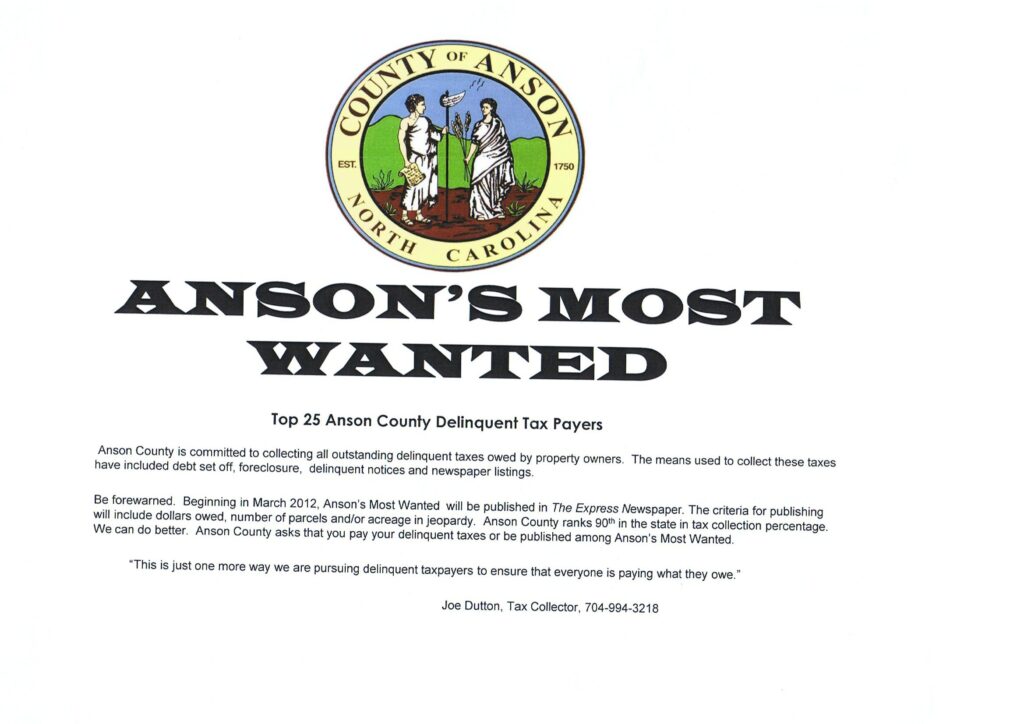

How creative can a tax collector be with the advertisement?

Many thanks to Anson County Tax Collector Joe Dutton for sharing the "most wanted" advertisement pictured above. Joe asked what I thought of his idea to run this ad and hopefully get the attention of some of his county’s largest delinquent taxpayers.

I told Joe I loved the ad, with a few caveats. As I explained in this post, just because the Machinery Act does not discuss “most wanted” ads or other similarly creative approaches to tax collection does not mean that such approaches are forbidden.

If tax collectors want to rent one of those huge digital billboards on I-40 to post the names of delinquent taxpayers for all to see, I think that would be perfectly legal. But those tax collectors could not pass along the cost of the billboard rentals to the delinquent taxpayers or use the billboards in lieu of the traditional newspaper ad for real property tax liens required by GS 105-369.

The same is true of Anson County’s “most wanted” ad. Joe will need to eat the cost of the “most wanted” ad and still run the traditional tax lien ad. But otherwise I think the ad passes legal muster.

Will Anson County’s ad ruffle some taxpayer feathers? Perhaps, but perhaps that is Joe’s goal. Shaking up taxpayer complacency might do wonders for the county’s tax collection rate. So long as the county commissioners don’t have problem with the ad, I don’t think Joe will either.

What do you think of Anson County’s ad? Use the comment section below to let me know your thoughts and about any creative collection ideas of your own.

What to do with taxpayers who pay just before the ad runs?

The typical notice of advertisement reads something like this: “Delinquent real property tax liens will be advertised on March 8. Failure to pay the delinquent taxes listed below before March 8 will result in your name being included in the list of delinquent taxpayers and you being charged a portion of the advertising cost.”

Problem is, if the ad will actually run on March 8 the newspaper will likely need the copy for that ad a day or two before March 8. Assume that the newspaper needs the final copy on March 6. If a taxpayer pays her delinquent taxes before March 6, then it is simple to resolve the situation: that taxpayer’s name is removed from the ad copy and the taxpayer will not be listed in the ad or charged a portion of the advertising cost.

But what if the taxpayer pays the delinquent taxes in the period between the submission of the final copy to the newspaper and the actual publication of the ad? This taxpayer will be less than thrilled if her name is included in the ad a few days later. And additional consternation may arise if she is charged a portion of that advertising cost despite the fact that she paid in full before the advertising date.

Assuming that it would be too late to remove the taxpayer’s name from the ad after the final copy has been submitted to the paper, I think the tax collector’s only option is to let the ad run but not to charge advertising costs to the formerly delinquent taxpayer. She’ll still suffer the negative publicity but at least won’t suffer additional financial penalty.

However, the best approach is to avoid this problem entirely by tweaking the language of the taxpayer notice. Instead of listing the actual publication date in the notice, consider providing as the payment deadline the date on which you need to submit the final ad copy.

In the example above, the notice could read, “Delinquent real property tax liens will be advertised on or after March 6. Failure to pay the delinquent taxes listed below before March 6 will result in your name being included in the list of delinquent taxpayers and you being charged a portion of the advertising cost.”

I think such a notice satisfies GS 105-369 while also providing taxpayers with a more accurate deadline to avoid negative publicity and additional costs.

Do newsstand purchasers count as "paid subscribers"?

To qualify as a newspaper of "general circulation" and therefore be an appropriate vehicle for tax lien advertisements, a newspaper must have more than a minimal number of "paid subscribers" sprinkled throughout the taxing jurisdiction. As a result, free newspapers published on the internet or newspapers available for free at newsstands and boxes cannot qualify for tax lien ads.

What about newspapers that are sold for 25 cents at newsstands and boxes across the county but have no subscribers who pay to receive their papers through the mail? I think the answer is no, those papers cannot qualify as newspapers of general circulation because a customer who buys a copy at a newsstand or box does not count as a paid subscriber. Both the courts and the statutes have made it clear that the emphasis is on subscribers rather than on readers when it comes time to determine which newspapers are appropriate publishers of tax liens and other public notices.

What does Austin Rivers’ buzzer beater against UNC have to do with tax advertisements?

Nothing at all. But I couldn’t possibly make it through this post without once mentioning Duke’s stunning win over the Heels last week. Go Devils!