The social justice protests that erupted in many areas of the country this summer focused mostly on law enforcement. But systemic bias can infect any area of government, even the seemingly objective world of property tax administration. For proof, check out the results of a large national property tax study released earlier this year:

Based on an analysis of 118 million home sales across the nation over the past ten years, the study concluded that Black-owned homes are more likely to be assessed at higher values relative to their sale price. In nearly every state, tax assessments were higher relative to sales prices in areas with higher Black and Hispanic populations.

Does this mean that our nation’s assessors and tax collectors are racist? Of course not. The fact that some government systems consistently produce results that are biased against minorities does not mean that the people who administer those systems are personally biased against minorities. Recognizing that systemic bias exists is not an accusation. It's a call to action. It creates an obligation on behalf of all of us involved in administering these systems to determine why these systems are producing unintentionally biased results and to make the changes necessary to minimize these biases.

My colleagues and I at the School of Government are committed to leading this effort. Shea Denning, director of the School's Judicial College, eloquently explained in this blog post how the School can help combat systemic racism in the judicial system. (Also take a look at this powerful video produced by the Judicial College: Reflections on Race and Justice.)

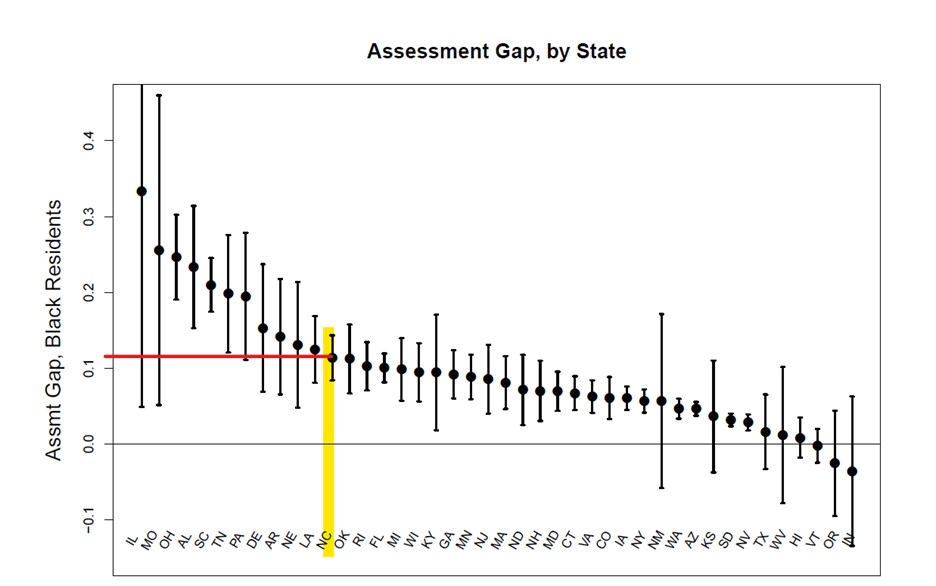

I promise to do the same in my areas of expertise. As a start, let’s take a closer look at the North Carolina data and results from that national property tax study. The “assessment gap” described in that study is the gap between the ratio of tax assessments to sales prices for Black-owned property as compared that same ratio for non-Black owned property. Overall, the study’s authors concluded that the assessment/sales ratios for Black-owned properties were 12.7% higher than the ratios for non-minority-owned properties.

The table below is reproduced from that study. North Carolina’s assessment gap (highlighted in yellow) was just over the.1 (10%) mark. (I added the red line to make it easier to see where NC fell on the scale.) In other words, Black-owned properties in NC were assessed 11-12% higher than white-owned properties as compared to actual sales prices. That result places NC just below the study’s average assessment gap of 12.7% but in the top third overall.

(From page 53 of this study.)

Our state's assessment gap could cost Black taxpayers dearly. Assume there are two houses in the city of Durham with identical market values of $200,000. One of those houses is owned by a white taxpayer and is assessed right at market value. The other house is owned by a Black taxpayer and is assessed at 11% above market value. Based on Durham’s current combined city/county tax rate, that gap would cause the Black taxpayer to pay about $270 more in taxes each year as compared to the white taxpayer.

Overt racism by individuals doing the assessing can’t be the driving force behind this gap, because assessors almost never know the races of property owners. Instead, the study suggests two structural problems as the primary causes of this gap.

The first problem is that market values vary over time more by neighborhood than do tax assessments. The study showed that identical houses in a given county are likely to have very similar tax assessments but often have very different market values based on the neighborhoods in which the houses reside. In other words, assessors appear to overestimating the expected growth in market value for many minority-majority neighborhoods. The second problem is that minority taxpayers are less likely to appeal their assessments than white taxpayers and are less likely to win when they do appeal. While the study bases this conclusion on data from only one county (Cook County, the home of Chicago and the second largest county in the U.S.), it seems likely this appeal disparity exists elsewhere.

I’m trying to access the specific NC data used in this study to learn more about the assessment gap in our state. I’d also like to work with NC assessors to see if we could recreate the Cook County study and determine if minority taxpayers disproportionately fail to benefit from the appeal process here in NC. Finally, I’d like to investigate other potential contributors to systemic bias in the administration of property taxes in NC, which might include:

- Lower participation in exemptions and exclusions by minority taxpayers;

- Fewer minority taxpayers taking advantage of property tax payment plans to avoid enforced collections; and,

- Foreclosure being used more frequently as a collection remedy in minority neighborhoods.

Assuming that there is evidence of systemic bias in North Carolina’s property tax, what can we do about it? I can think of two approaches, one aimed at assessors and one aimed at taxpayers.

First, make more assessors aware of these unintentionally biased results, which will encourage assessors to be more alert to potential causes. For example, my appraisal expert colleague Kirk Boone suggests that assessors place more emphasis on “vertical equity” to ensure that less expensive properties are assessed just as close to market value as are more expensive properties. Assessors might also take second or third looks at the assessments in minority-majority neighborhoods to make sure they accurately reflect hyper-local market conditions. Finally, assessors might recommend more frequent county-wide reappraisals (perhaps every four years instead of every eight), which could help remedy disparate gaps between assessments and sales prices.

Second, improve outreach to minority taxpayers. A systemic bias might reflect an information gap; minority taxpayers might not know as much about exclusions, payment plans, and the appeal process as do white taxpayers. Assuring minority taxpayers that applying for exclusions and appealing their assessments is relatively easy (no lawyers needed!) and will not subject them and their families to excessive government scrutiny (police will not suddenly appear at their doors) might encourage more minority taxpayers to take advantage of these processes. While in the short term this outreach would create more work for tax staff, in the long run it would make assessments more accurate and more fairly distribute the property tax burden across the county.

I look forward to working with property tax officials across our state to identify and minimize systemic biases in our property tax system. I welcome your suggestions about how we can accomplish this vital goal together.